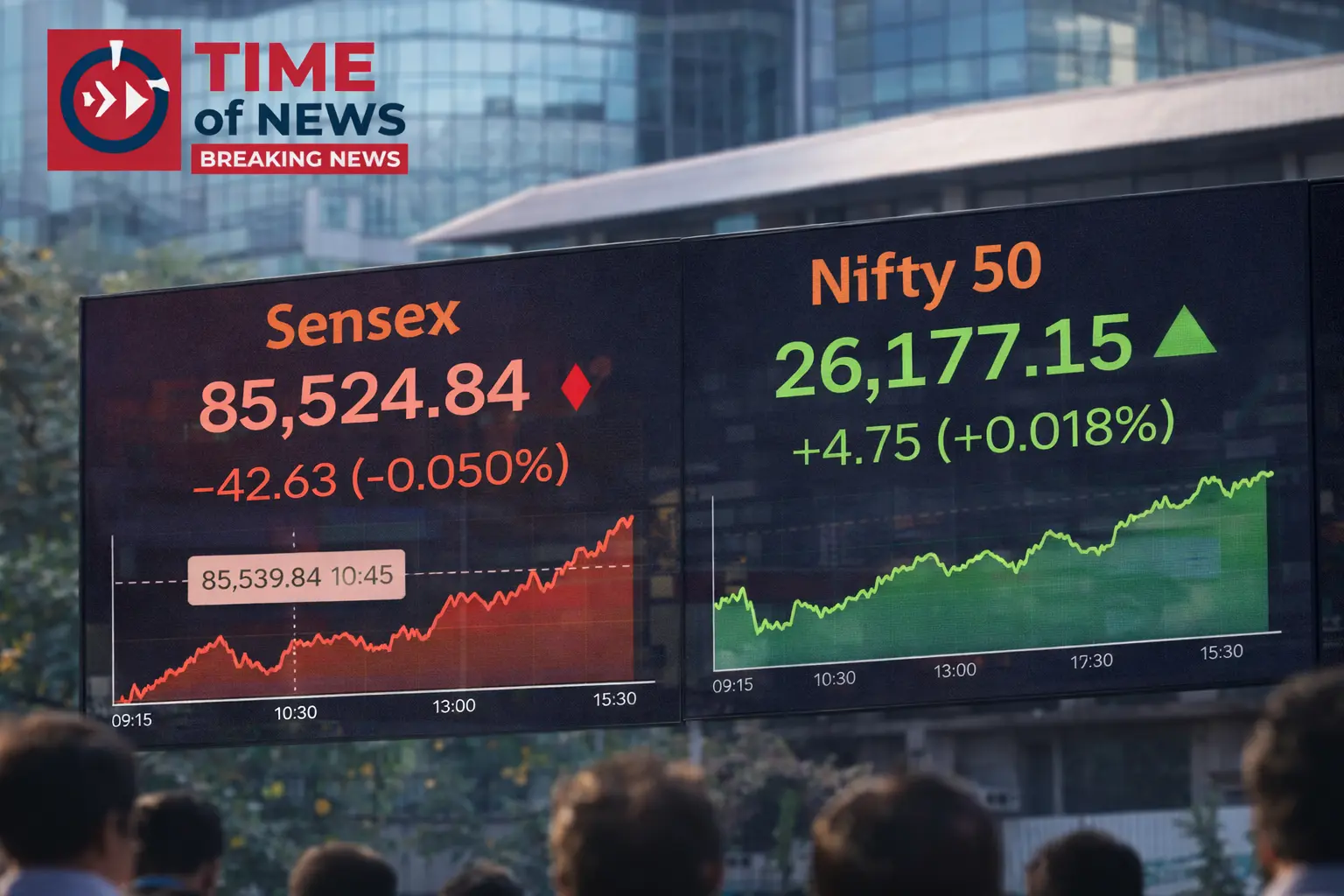

India has achieved a historic economic milestone by overtaking Japan to become the world’s fourth-largest economy. Strong growth, stable inflation, and rising investment have powered this global rise

India has officially emerged as the world’s fourth-largest economy, surpassing Japan in total Gross Domestic Product (GDP), according to the Indian government’s latest end-of-year economic assessment.

With an estimated GDP of around $4.18 trillion, India now ranks just behind the United States, China, and Germany, marking a significant leap in the country’s global economic standing.

Strong Growth Drives India’s Rise

Economists attribute this achievement to robust domestic demand, increased capital investment, infrastructure expansion, and controlled inflation. Despite global economic uncertainty, India has maintained steady growth momentum across manufacturing, services, and technology sectors.

Government officials believe that continued reforms, digital transformation, and policy stability will keep India on a strong growth trajectory in the coming years.

India Could Soon Become the Third-Largest Economy

Looking ahead, policymakers project that India could overtake Germany within the next 2.5 to 3 years, potentially becoming the world’s third-largest economy if current trends continue.

Why This Milestone Matters

• Strengthens India’s position in the global economic order

• Boosts investor confidence and foreign direct investment (FDI)

• Enhances India’s influence in international economic and policy forums

• Reflects the resilience of the Indian economy amid global challenges

A Defining Moment for India

This achievement is seen as a defining moment in India’s economic journey, highlighting the country’s growing role as a global growth engine and reinforcing optimism about its long-term economic future